영국 영란은행 기준금리동결-20200618

FOHUNTERS™

FOHUNTERS™

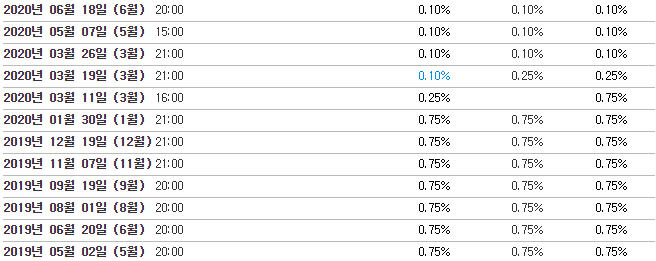

| 기준금리 | 0.10% |

|---|

20시에 발표되었던 내용입니다.

Bank Rate maintained at 0.1% - June 2020

Our MPC voted unanimously to maintain Bank Rate at 0.1% and to continue with the existing programme of £200 billion of UK government bond and sterling non-financial investment-grade corporate bond purchases, financed by the issuance of central bank reserves. The Committee voted by a majority of 8-1 to increase the target stock of purchased UK government bonds, financed by the issuance of central bank reserves, by an additional £100 billion, to take the total stock of asset purchases to £745 billion.

Monetary Policy Summary and minutes of the Monetary Policy Committee meeting

Current Bank Rate0.1%

Next due: 6 August 2020

Published on 18 June 2020

The Bank of England’s Monetary Policy Committee (MPC) sets monetary policy to meet the 2% inflation target, and in a way that helps to sustain growth and employment. In that context, its challenge at present is to respond to the severe economic and financial disruption caused by the spread of Covid-19. At its meeting ending on 17 June 2020, the MPC voted unanimously to maintain Bank Rate at 0.1%. The Committee voted unanimously for the Bank of England to continue with the existing programme of £200 billion of UK government bond and sterling non-financial investment-grade corporate bond purchases, financed by the issuance of central bank reserves. The Committee voted by a majority of 8-1 for the Bank of England to increase the target stock of purchased UK government bonds, financed by the issuance of central bank reserves, by an additional £100 billion, to take the total stock of asset purchases to £745 billion.

Risky asset prices have recovered further from their March lows, although they have remained sensitive to news on the evolution of the pandemic. Recent data outturns suggest that the fall in global GDP in 2020 Q2 will be less severe than expected at the time of the May Monetary Policy Report. There are signs of consumer spending and services output picking up, following the easing of Covid-related restrictions on economic activity. Recent additional announcements of easier monetary and fiscal policy will help to support the recovery. Downside risks to the global outlook remain, however, including from the spread of Covid-19 within emerging market economies and from a return to a higher rate of infection in advanced economies.

UK GDP contracted by around 20% in April, following a 6% fall in March. Evidence from more timely indicators suggests that GDP started to recover thereafter. Payments data are consistent with a recovery in consumer spending in May and June, and housing activity has started to pick up recently. The LFS unemployment rate was unchanged at 3.9% in the three months to April. But other and more timely indications from the claimant count, HMRC payrolls data and job vacancies suggest that the labour market has weakened materially. Following stronger than expected take-up of the Coronavirus Job Retention Scheme, a greater number of workers are likely to be furloughed in the second quarter. Evidence from business surveys and the Bank’s Agents is consistent with a weak outlook for employment in coming quarters. Some households are also worried about their job security.

Twelve-month CPI inflation declined from 1.5% in March to 0.8% in April, triggering the explanatory letter from the Governor to the Chancellor published alongside this monetary policy announcement. CPI inflation fell further in May, to 0.5%. Current below-target rates of CPI inflation can in large part be accounted for by the effects of the pandemic. The collapse in global oil prices has had direct effects on inflation, via the prices of motor fuels, and indirect effects by reducing input costs in other sectors of the economy. The sharp drop in domestic activity is also adding to downward pressure on inflation through increased spare capacity in most sectors of the economy.

The unprecedented situation means that the outlook for the UK and global economies is unusually uncertain. It will depend critically on the evolution of the pandemic, measures taken to protect public health, and how governments, households and businesses respond to these factors.

The emerging evidence suggests that the fall in global and UK GDP in 2020 Q2 will be less severe than set out in the May Report. Although stronger than expected, it is difficult to make a clear inference from that about the recovery thereafter. There is a risk of higher and more persistent unemployment in the United Kingdom. Even with the relaxation of some Covid-related restrictions on economic activity, a degree of precautionary behaviour by households and businesses is likely to persist. The economy, and especially the labour market, will therefore take some time to recover towards its previous path. CPI inflation is well below the 2% target and is expected to fall further below it in coming quarters, largely reflecting the weakness of demand.

At this meeting, the MPC judges that a further easing of monetary policy is warranted to meet its statutory objectives. The Committee agreed to increase the target stock of purchased UK government bonds by an additional £100 billion in order to meet the inflation target in the medium term. The Committee expects that programme to be completed, and the total stock of asset purchases to reach £745 billion, around the turn of the year.

The MPC will continue to monitor the situation closely and, consistent with its remit, stands ready to take further action as necessary to support the economy and ensure a sustained return of inflation to the 2% target. The Committee will keep the asset purchase programme under review.